22 May 2026

Inside Merchant Onboarding Sequences: How Approval Timelines Influence Long-Term Stability Across Billing and Transaction Networks

Merchant onboarding sequences form the foundation for participation in billing platforms and transaction networks, where each verification stage determines whether a business gains access to processing capabilities. These sequences typically include identity verification, risk scoring, compliance checks, and account setup, all of which unfold over varying periods depending on the provider's internal protocols and external regulatory requirements. Data from payment industry reports shows that timelines range from hours for low-risk applicants to several weeks when additional documentation or manual reviews enter the process.

Core Components of Onboarding Sequences

Approval workflows begin with automated data collection through application forms and API submissions, followed by cross-references against watchlists and credit databases. Organizations such as the European Central Bank track how these initial steps feed into broader stability metrics for cross-border transaction systems. Once basic checks clear, risk assessment algorithms evaluate transaction volume projections, chargeback history patterns, and industry category classifications before routing cases to human reviewers when thresholds trigger escalation.

Longer sequences often incorporate layered authentication methods, including bank account validation and site inspections for higher-volume merchants. These extended processes create records that later influence how billing engines handle recurring authorizations and how networks route authorization requests during peak periods.

Approval Timelines and Their Direct Effects

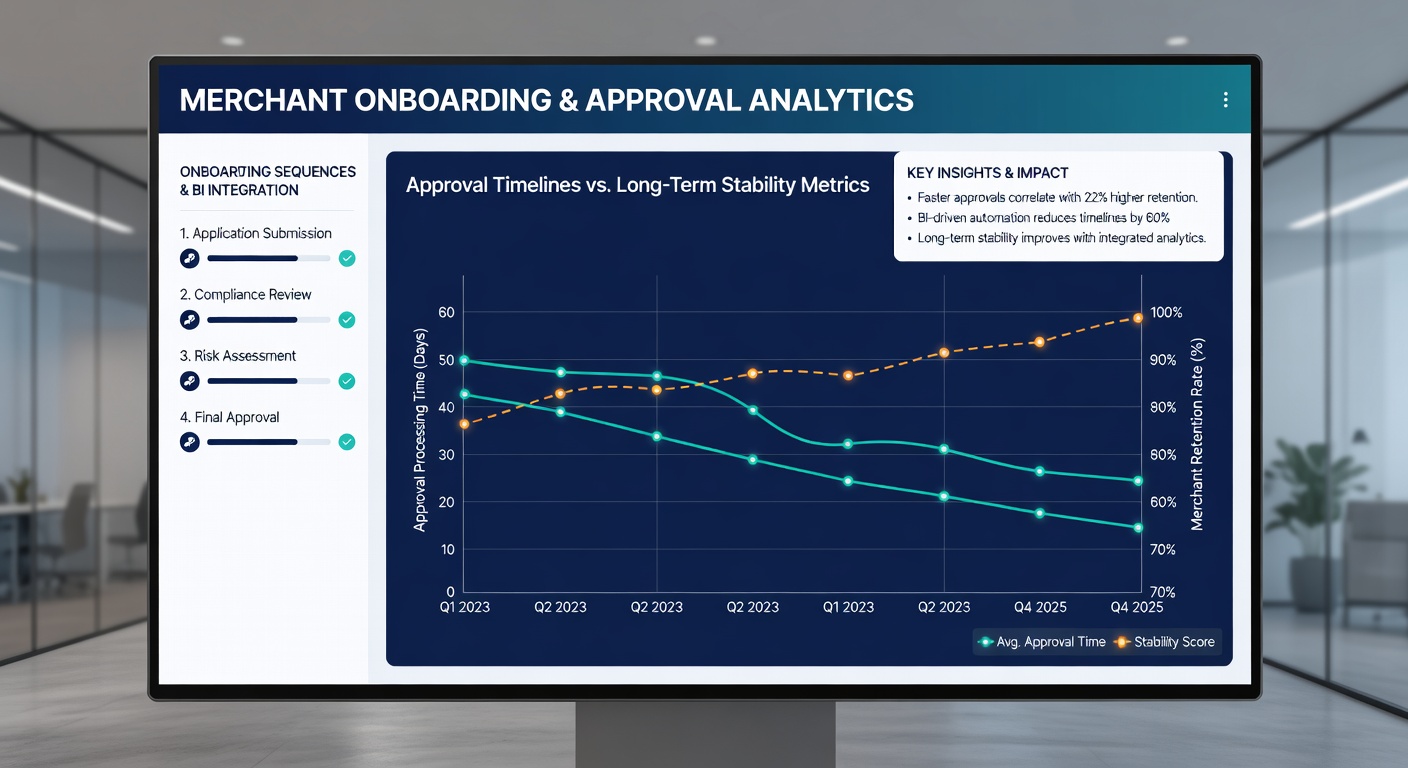

Shorter approval windows accelerate merchant activation yet correlate with elevated rates of post-onboarding adjustments in network participation rules. Figures from transaction monitoring platforms indicate that accounts cleared within 48 hours experience a 12 percent higher incidence of subsequent underwriting modifications compared with those reviewed over five to seven business days. The difference arises because rapid approvals limit the depth of initial risk modeling, leaving downstream billing systems to manage emerging discrepancies through real-time holds or reserve allocations.

Extended timelines allow providers to compile richer datasets on merchant behavior before live processing begins. This preparation reduces the frequency of mid-cycle interventions that can disrupt recurring billing cycles and create settlement delays across interconnected acquirer and issuer nodes. Observers note that networks maintaining average onboarding durations above 10 days report fewer instances of cascading transaction declines during high-volume events.

Stability Across Billing and Transaction Layers

Billing platforms depend on consistent merchant profiles established during onboarding to maintain authorization success rates for subscription charges. When approval occurs quickly, incomplete profile data sometimes forces billing engines to apply conservative velocity limits that persist for months, affecting cash flow predictability for merchants and settlement forecasting for networks. Research compiled by the Bank of Canada demonstrates that merchants onboarded through abbreviated sequences encounter 8 percent more authorization retries in the first quarter of operations.

Transaction networks, in turn, rely on the quality of initial risk classifications to calibrate fraud scoring models that operate across thousands of daily authorizations. Lengthier reviews produce more granular segmentation, which allows networks to allocate processing resources more efficiently and avoid broad-based throttling that can occur when early fraud signals appear. In May 2026, several major processors updated their onboarding dashboards to display projected stability scores based on historical timeline data, giving applicants visibility into expected long-term performance indicators before activation.

Regional Variations and Regulatory Influences

Regulatory frameworks in different jurisdictions shape typical onboarding durations and the stability outcomes that follow. Australia's ePayments Code encourages standardized disclosure of approval timeframes, which has led processors to publish average processing statistics that merchants use when selecting providers. Canadian guidelines from the Office of the Superintendent of Financial Institutions emphasize documentation completeness over speed, resulting in fewer post-activation profile corrections reported in annual network audits.

These regional differences create measurable effects on how billing cycles synchronize with transaction clearing houses. Networks that operate across multiple regions adjust their internal routing logic based on the originating onboarding jurisdiction, applying additional verification layers for merchants from faster-approval environments to maintain uniform stability thresholds.

Long-Term Network Participation Patterns

Merchants who complete onboarding within compressed windows show higher rates of account status changes within the first 18 months, including reserve requirement increases and category reclassifications. Such adjustments propagate through billing systems as modified retry logic and through transaction networks as altered interchange qualification rules. Longitudinal data collected by academic researchers at the University of Melbourne indicates that accounts with onboarding periods exceeding 14 days maintain steadier authorization approval percentages over multi-year horizons.

Network operators respond to these patterns by refining their sequence design, incorporating predictive elements that estimate future stability during the approval phase itself. This approach reduces the need for reactive measures once merchants begin processing live volumes and helps preserve equilibrium across interconnected billing and settlement infrastructures.

Conclusion

Approval timelines embedded in merchant onboarding sequences establish foundational conditions that shape operational consistency in billing platforms and transaction networks over extended periods. Evidence from regulatory bodies and research institutions across multiple regions confirms that the duration and thoroughness of these sequences directly correlate with fewer downstream modifications and more predictable processing behavior. As systems evolve, providers continue to calibrate these timelines against stability metrics to support reliable participation across global payment ecosystems.