2 Jun 2026

Mapping Authorization Pathways for High-Risk Merchants Through Layered Verification Layers in Niche Retail Sectors

High-risk merchants operating in niche retail sectors encounter distinct authorization challenges that standard payment processes often fail to address adequately, and mapping those pathways requires systematic application of multiple verification layers to maintain transaction integrity. Niche categories such as specialty electronics, certain health supplements, or limited-run apparel lines carry elevated chargeback probabilities according to industry data compiled through 2025, which forces processors to construct authorization sequences that evaluate risk at successive checkpoints rather than relying on single-point approvals.

Identifying High-Risk Profiles in Specialized Retail

Processors classify merchants as high-risk when transaction patterns show elevated dispute rates, product categories trigger regulatory scrutiny, or business models involve recurring billing elements that complicate consumer consent verification. Data from multiple payment networks reveals that niche retail segments experience chargeback ratios between 1.8 and 4.2 percent, figures that exceed general retail averages and prompt the deployment of additional verification steps during onboarding and ongoing transaction routing. Observers note that businesses selling customized goods or operating in jurisdictions with strict consumer protection rules frequently receive this designation because their sales cycles extend longer than typical e-commerce flows.

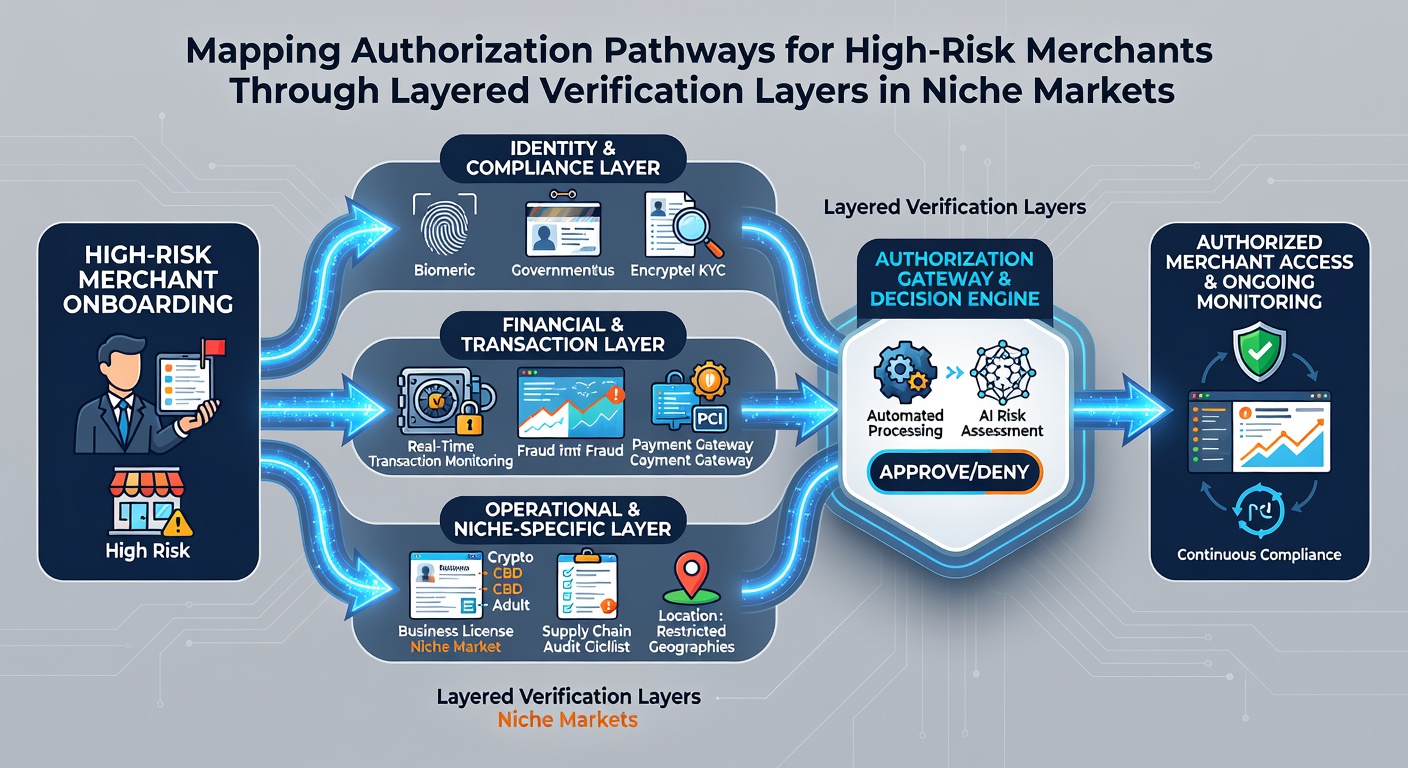

Constructing Layered Verification Structures

Authorization pathways for these merchants rely on sequential verification layers that begin with identity confirmation and progress through transaction pattern analysis, device fingerprinting, and velocity checks before final approval occurs. Each layer operates independently yet feeds data into a central decision engine, which allows processors to adjust thresholds dynamically based on real-time signals rather than static rules. Research from payment security consortia indicates that multi-layer systems reduce unauthorized approvals by 37 percent compared with single-layer models when applied consistently across high-risk portfolios. The first layer typically validates business registration and ownership documentation, while subsequent layers examine historical transaction data, geographic inconsistencies, and customer behavior metrics collected at the point of sale.

Tracing Authorization Flows Through Decision Points

Mapping begins by documenting every decision node where an authorization request encounters a verification gate, and this documentation captures both automated rules and manual review triggers that activate when scores exceed predefined limits. In practice, a request might pass initial merchant credential checks only to encounter a secondary layer that cross-references customer IP data against known high-risk regions, then move to a third layer evaluating order value against historical averages for that specific merchant category. Processors update these maps quarterly because regulatory changes and emerging fraud tactics alter the effectiveness of individual layers, and June 2026 updates are expected to incorporate new requirements around biometric consent verification in several jurisdictions.

Application in Distinct Niche Retail Environments

Niche sectors such as artisanal food imports and performance equipment suppliers illustrate how layered pathways adapt to unique operational constraints, since these categories often involve higher average ticket sizes and international shipping variables that increase dispute likelihood. Verification sequences in these environments integrate customs documentation checks alongside standard payment data, which creates additional decision branches that standard retail pathways do not require. Reports from the Consumer Financial Protection Bureau document that merchants handling cross-border specialty goods experience 22 percent more verification escalations than domestic-only counterparts, prompting processors to insert dedicated compliance layers before funds capture. Another source, a 2025 study released through the Australian Securities and Investments Commission, highlights similar patterns among merchants dealing in restricted-substance retail products where verification must also satisfy therapeutic goods regulations.

Adjusting Pathways Based on Performance Metrics

Continuous monitoring allows processors to refine layer weights when certain verification steps generate disproportionate false declines, and this adjustment process relies on aggregated performance data rather than individual transaction outcomes. Merchants that demonstrate consistent compliance over six-month periods sometimes receive pathway simplifications that reduce the number of active layers while preserving overall risk controls. Evidence from network-level analytics shows that such calibrated reductions maintain chargeback rates within acceptable bands provided the remaining layers retain strong predictive power. Those who manage these systems emphasize that mapping remains an iterative task because fraud patterns evolve and regulatory expectations shift, particularly as new reporting standards take effect in multiple regions during 2026.

Conclusion

Effective mapping of authorization pathways through layered verification provides high-risk merchants in niche retail with structured access to payment networks while containing exposure for processors and card networks alike. The approach combines identity, behavioral, and compliance checks into coherent sequences that adapt to category-specific risks and jurisdictional requirements. Ongoing refinement based on performance data ensures these pathways remain functional as market conditions and regulatory frameworks continue to develop.